Computing a sparse solution of a set of linear inequalities¶

A derivative work by Judson Wilson, 5/11/2014. Adapted from the CVX example of the same name, by Almir Mutapcic, 2/28/2006.

Topic References:

Section 6.2, Boyd & Vandenberghe “Convex Optimization”

“Just relax: Convex programming methods for subset selection and sparse approximation” by J. A. Tropp

Introduction¶

We consider a set of linear inequalities \(Ax \preceq b\) which are feasible. We apply two heuristics to find a sparse point \(x\) that satisfies these inequalities.

The (standard) \(\ell_1\)-norm heuristic for finding a sparse solution is:

The log-based heuristic is an iterative method for finding a sparse solution, by finding a local optimal point for the problem:

where \(\delta\) is a small threshold value (which determines if a value is close to zero). We cannot solve this problem since it is a minimization of a concave function and thus it is not a convex problem. However, we can apply a heuristic in which we linearize the objective, solve, and re-iterate. This becomes a weighted \(\ell_1\)-norm heuristic:

which in each iteration re-adjusts the weights \(W_i\) based on the rule:

where \(\delta\) is a small threshold value.

This algorithm is described in papers:

“An affine scaling methodology for best basis selection” by B. D. Rao and K. Kreutz-Delgado

“Portfolio optimization with linear and fixed transaction costs” by M. S. Lobo, M. Fazel, and S. Boyd

Generate problem data¶

import cvxpy as cp

import numpy as np

# Fix random number generator so we can repeat the experiment.

np.random.seed(1)

# The threshold value below which we consider an element to be zero.

delta = 1e-8

# Problem dimensions (m inequalities in n-dimensional space).

m = 100

n = 50

# Construct a feasible set of inequalities.

# (This system is feasible for the x0 point.)

A = np.random.randn(m, n)

x0 = np.random.randn(n)

b = A.dot(x0) + np.random.random(m)

\(\ell_1\)-norm heuristic¶

# Create variable.

x_l1 = cp.Variable(shape=n)

# Create constraint.

constraints = [A*x_l1 <= b]

# Form objective.

obj = cp.Minimize(cp.norm(x_l1, 1))

# Form and solve problem.

prob = cp.Problem(obj, constraints)

prob.solve()

print("status: {}".format(prob.status))

# Number of nonzero elements in the solution (its cardinality or diversity).

nnz_l1 = (np.absolute(x_l1.value) > delta).sum()

print('Found a feasible x in R^{} that has {} nonzeros.'.format(n, nnz_l1))

print("optimal objective value: {}".format(obj.value))

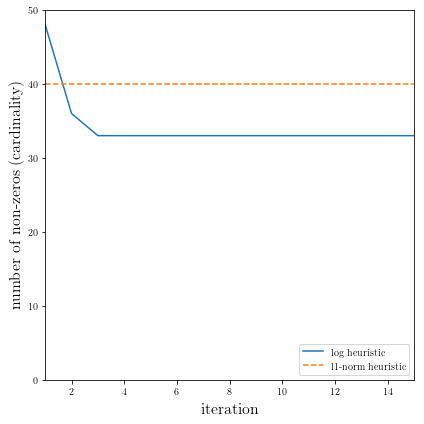

status: optimal

Found a feasible x in R^50 that has 40 nonzeros.

optimal objective value: 28.582394099513873

Iterative log heuristic¶

# Do 15 iterations, allocate variable to hold number of non-zeros

# (cardinality of x) for each run.

NUM_RUNS = 15

nnzs_log = np.array(())

# Store W as a positive parameter for simple modification of the problem.

W = cp.Parameter(shape=n, nonneg=True);

x_log = cp.Variable(shape=n)

# Initial weights.

W.value = np.ones(n);

# Setup the problem.

obj = cp.Minimize( W.T*cp.abs(x_log) ) # sum of elementwise product

constraints = [A*x_log <= b]

prob = cp.Problem(obj, constraints)

# Do the iterations of the problem, solving and updating W.

for k in range(1, NUM_RUNS+1):

# Solve problem.

# The ECOS solver has known numerical issues with this problem

# so force a different solver.

prob.solve(solver=cp.CVXOPT)

# Check for error.

if prob.status != cp.OPTIMAL:

raise Exception("Solver did not converge!")

# Display new number of nonzeros in the solution vector.

nnz = (np.absolute(x_log.value) > delta).sum()

nnzs_log = np.append(nnzs_log, nnz);

print('Iteration {}: Found a feasible x in R^{}'

' with {} nonzeros...'.format(k, n, nnz))

# Adjust the weights elementwise and re-iterate

W.value = np.ones(n)/(delta*np.ones(n) + np.absolute(x_log.value))

Iteration 1: Found a feasible x in R^50 with 48 nonzeros...

Iteration 2: Found a feasible x in R^50 with 36 nonzeros...

Iteration 3: Found a feasible x in R^50 with 33 nonzeros...

Iteration 4: Found a feasible x in R^50 with 33 nonzeros...

Iteration 5: Found a feasible x in R^50 with 33 nonzeros...

Iteration 6: Found a feasible x in R^50 with 33 nonzeros...

Iteration 7: Found a feasible x in R^50 with 33 nonzeros...

Iteration 8: Found a feasible x in R^50 with 33 nonzeros...

Iteration 9: Found a feasible x in R^50 with 33 nonzeros...

Iteration 10: Found a feasible x in R^50 with 33 nonzeros...

Iteration 11: Found a feasible x in R^50 with 33 nonzeros...

Iteration 12: Found a feasible x in R^50 with 33 nonzeros...

Iteration 13: Found a feasible x in R^50 with 33 nonzeros...

Iteration 14: Found a feasible x in R^50 with 33 nonzeros...

Iteration 15: Found a feasible x in R^50 with 33 nonzeros...

Result plots¶

The following code plots the result of the \(\ell_1\)-norm heuristic, as well as the result for each iteration of the log heuristic.

import matplotlib.pyplot as plt

# Show plot inline in ipython.

%matplotlib inline

# Plot properties.

plt.rc('text', usetex=True)

plt.rc('font', family='serif')

plt.figure(figsize=(6,6))

# Plot the two data series.

plt.plot(range(1,1+NUM_RUNS), nnzs_log, label='log heuristic')

plt.plot((1, NUM_RUNS), (nnz_l1, nnz_l1), linestyle='--', label='l1-norm heuristic')

# Format and show plot.

plt.xlabel('iteration', fontsize=16)

plt.ylabel('number of non-zeros (cardinality)', fontsize=16)

plt.ylim(0,n)

plt.xlim(1,NUM_RUNS)

plt.legend(loc='lower right')

plt.tight_layout()

plt.show()